MBW Reacts is a sequence of quick remark items from the MBW group. They’re our ‘fast take’ reactions – by a music biz lens – to main leisure information tales.

Spotify‘s institutional shareholders – Common Music Group amongst them – can’t be finest happy.

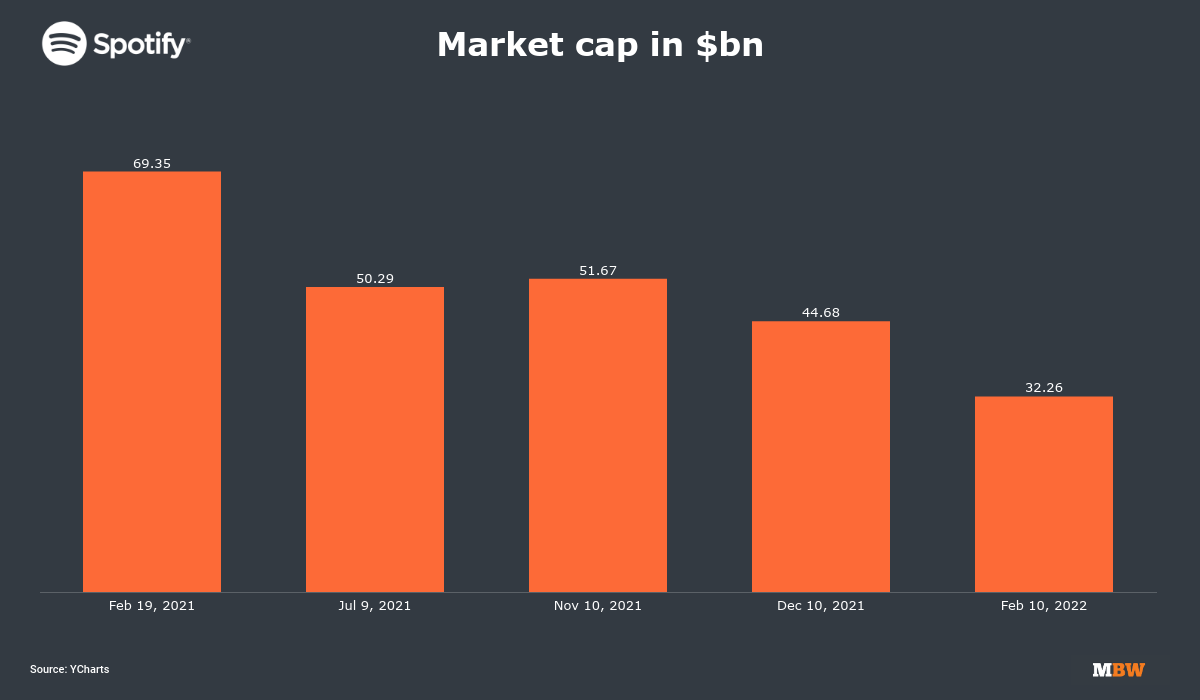

The streaming service’s share value, and due to this fact its market cap valuation, has plummeted by greater than 50% over the previous 12 months.

On the time of writing (on February 10), in keeping with YCharts, Spotify’s market cap worth on the New York Inventory Alternate sits at $32.26 billion.

That’s lower than half the scale of the place it was at its peak within the prior yr, on February 19, 2020: $69.35 billion.

The explanations behind this collapse in Spotify’s share value are quite a few. However the broadly subscribed-to concept that it’s all merely a part of a wave of tech shares taking a hammering is a misnomer.

For instance, Apple‘s share value in the identical interval (February 19, 2021 by February 10, 2022) has grown by a 3rd (+33%).

Certainly, the Dow Jones US Expertise Index, which tracks the inventory efficiency of US firms within the know-how business, has itself grown by 17.9% in the identical time interval.

The concept the Neil Younger vs. Joe Rogan fracas has sunk Spotify’s share value is equally over-baked.

It is true that Spotify’s market cap tumbled pretty dramatically within the days following the removing of Neil Younger’s music from the service (January 26).

However SPOT’s share value is definitely now again to pre-Younger-fallout ranges: Final month, at buying and selling shut on the day Younger’s music got here down, Spotify’s share value was at $174.79; it closed yesterday (February 9) at $175.49.

Analysts usually stay constructive on the prospects for Spotify’s inventory – simply not essentially as constructive as they as soon as have been.

The likes of Guggenheim’s Michael Morris, BOFA’s Jessica Erlich, Truist Securities’ Matthew Thornton, and Rosenblatt Securities’ Mark Zgutowicz have all not too long ago reiterated their view of Spotify as a ‘Purchase’.

Nevertheless, every of them has additionally lowered their value expectation for SPOT inventory.

Actually, not all analysts responded favorably to a few of Spotify’s bulletins inside its This autumn 2021 outcomes final week.

That’s very true of the information that Spotify provided softer steerage than analyst expectations for each (i) Q1 2022 premium subs additions (SPOT’s anticipating 3 million new subs this quarter; analysts wished to see 4 million), and (ii) Q1 2022 gross revenue margin.

In fact, there was a whole lot of very constructive information in Spotify’s This autumn 2021 outcomes.

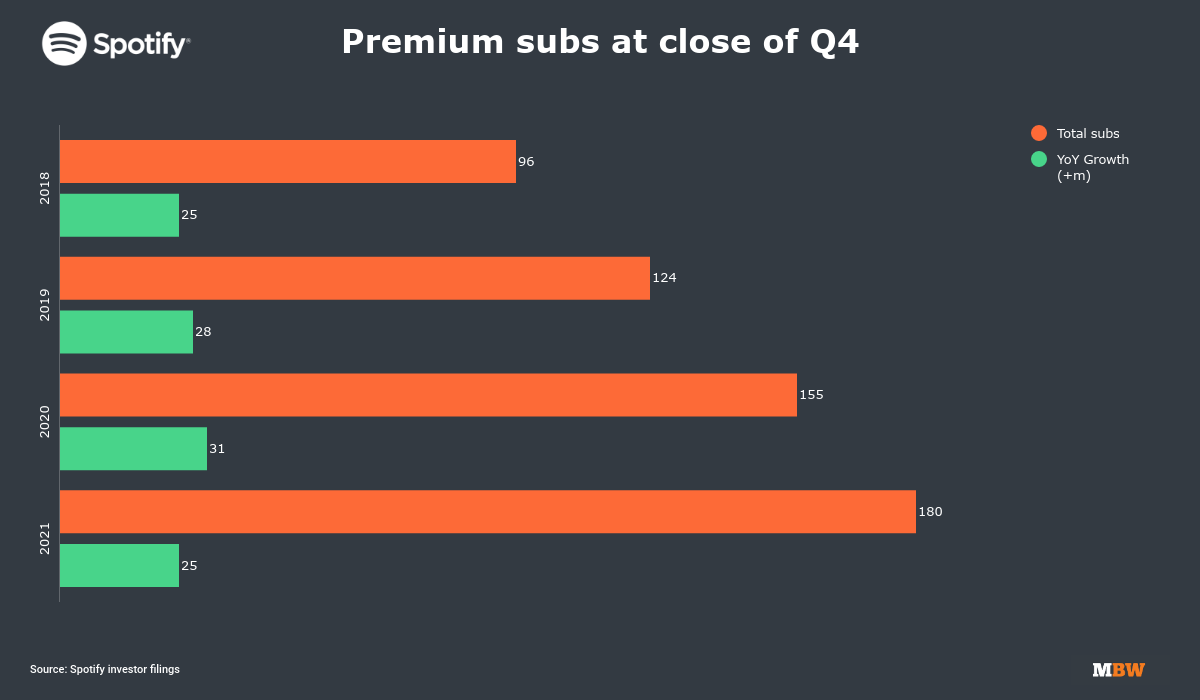

Sure, the corporate’s annual subscriber development in 2021 was slower than it was within the earlier two years (see under).

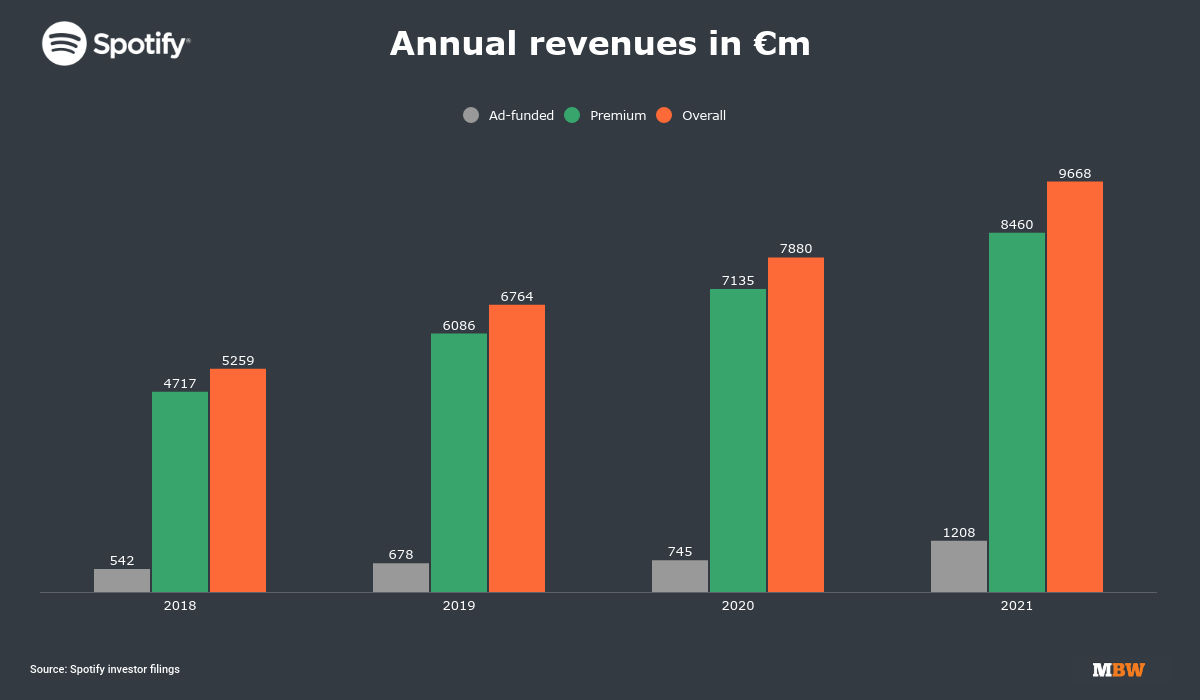

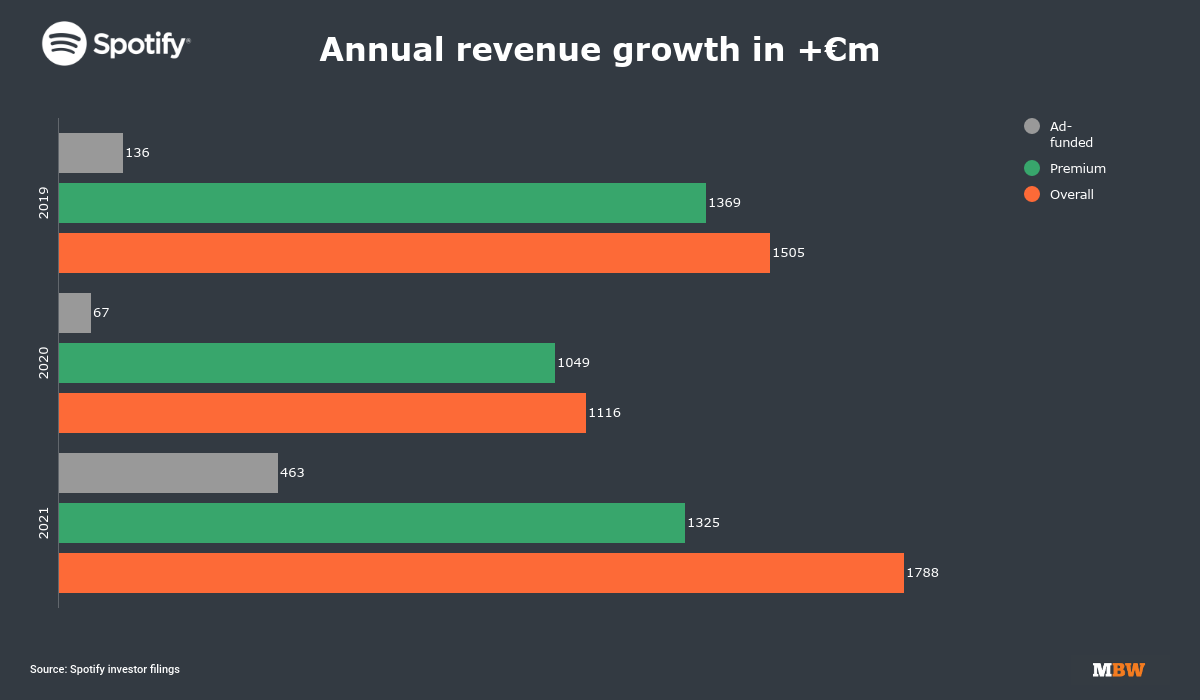

However Spotify’s annual subscriber income development in 2021 was truly bigger than it was in every of 2020 and 2019.

In different phrases, Spotify added fewer subscribers than it did within the prior yr, however (presumably because of gentle value rises in sure territories) the cumulative quantity these subscribers truly paid shot up.

As well as, Spotify’s complete Month-to-month Lively Customers (MAUs) grew by 61 million YoY in 2021, as much as a year-end complete of 408 million.

In brief, then: Spotify seems on track to blast by 200 million paying international subs this yr, and crash by the half-billion Month-to-month Lively Customers barrier within the subsequent 24 months.

As well as, its premium subscription income development is accelerating, whereas its adverts enterprise is (comparatively) exploding – up €463 million year-on-year in 2021.

Complaints round gross margin and subscriber steerage apart, there’s rather a lot to admire right here for each traders and the music enterprise – which explains why so many analysts (70% of them, in keeping with eToro) proceed to see Spotify inventory as a ‘Purchase’.

This mix of things, nevertheless (Spotify’s share value being slashed in half inside a yr, alongside wholesome subs, income and consumer development in 2021) has led to a few speculators whispering whispers in MBW’s course this week.

Probably the most audacious of those wonderings: May one in every of Large Tech’s titans be tempted to make a shock cut-price acquisition play for Spotify within the months forward?

This clearly stays a extremely unlikely state of affairs; the regulatory headache for an Alphabet or Apple, to call however two, would very presumably snuff out even the remotest probability of an acquisitive inquiry from both of them.

Nevertheless it’s not unimaginable – and there’s no denying the potential value-add that Spotify’s 180 million-plus paying subscribers would deliver to one in every of its direct rivals.

In line with Midia Analysis, for instance, Apple Music had round 79 million international subscribers in Q2 2021.

A mixed Apple and Spotify, then, would simply surpass 1 / 4 of a billion worldwide subscribers immediately.

Wanting outdoors of music streaming’s Large Tech gamers introduces a few even wilder wildcard concepts.

Take, for instance, Microsoft, which simply agreed a $69 billion deal to purchase gaming large Activision Blizzard (like Spotify, a publicly traded enterprise).

Like Spotify, Activision Blizzard – primarily as a consequence of accusations of dreadful office misconduct – noticed its worth slide dramatically over the previous yr (earlier than Microsoft’s acquisition announcement, that’s).

Activision Blizzard’s market cap was almost reduce in half between February 12 final yr ($80.37 billion) and December 3 ($44.68 billion).

There’s a honest argument that Microsoft took swift benefit of this collapse in Activision Blizzard’s worth with its shock buyout.

May Spotify’s equally steep fall in market cap tempt any consideration of the same transfer?

One other enjoyable suggestion for you: Netflix.

The video streaming large has seen its inventory worth decline by almost 25% prior to now month, following the revelation of disappointing subscriber development in its This autumn 2021 outcomes.

Netflix informed traders final month that it now expects to add simply 2.5 million new subs to its service in Q1 2022 – considerably under the three.98 million analysts anticipated it so as to add.

What might the addition of Spotify’s 180 million-plus Premium subscriber base do to Netflix’s international subscription enterprise… and to the fortunes of its share value?

For now, chalk all this down as merely a little bit of enjoyable sprinkled with some kernels of foolish hypothesis.

Except it ever turns into actual, that’s.

Then MBW will inform you, repeatedly and straight-faced, that we referred to as it early proper right here.Music Enterprise Worldwide

{kind=link}