The forthcoming US CPI information are anticipated to point that inflation continued to rise in April, albeit at a slower price than in earlier months. The Bloomberg survey of consultants forecasts an 8.1% enhance in US client costs following March’s 8.5% enhance. That is the primary decline in inflation since August 2021. Additionally it is anticipated that the “core” CPI, which removes the affect of volatility within the power and meals sectors, may have slowed in April in comparison with the identical month final yr. Nevertheless, a report anticipated on Wednesday might reveal that core inflation has risen from the earlier month.

Greg McBride, chief monetary analyst at Bankrate, believes that home costs warrant shut consideration. He acknowledged that housing represents 40% of the CPI, as do family budgets, and that this, along with double-digit lease hikes, strains family budgets even when meals and power costs stay secure. Along with this CPI report, the US Federal Reserve is predicted to ponder an extra enhance in rates of interest of 0.5 foundation factors at its June assembly. Consequently, the Fed’s computation might deviate considerably from its CPI projection if the CPI divergence is appreciable in both route.

As a result of fast rise in inflation, the US Federal Reserve has been compelled to aggressively increase rates of interest and deleverage its steadiness sheet by $8.9 trillion. Consequently, equities are at the moment in correction space or a bear market. Inflation was largely brought on by issues with the provision chain and rising demand on account of the outbreak.

We will study the April client value estimate on Wednesday, previous to the opening of the inventory markets. The proportion of all gadgets is anticipated to say no from 8.5% to 8.1%. In comparison with March of the earlier yr, power costs elevated by 32% in March. Diesel and gasoline costs have been almost regular in April, which is able to assist restrain inflationary pressures, on condition that they account for round 4% of the CPI, and climbed 48.2% year-over-year in March.

How a lot did UK GDP develop within the first quarter?

Following the removing of all Covid-19 limitations earlier this yr, the Financial institution of England forecasts a first-quarter enlargement of 0.9% for the British economic system. Based on Reuters, economists predict that the gross home product might climb by 1% throughout the quarter for which information will likely be revealed on Thursday. Throughout this era, manufacturing can be anticipated to extend by 0.1%. This might affirm the 0.1% development price in February, which decreased from 0.8% in January. Ellie Henderson, an economist at Investec, forecasts that financial enlargement will resume. Nevertheless, manufacturing and development are anticipated to lower in March, whereas companies are projected to extend by 0.1%. In consequence, covid immunisation will likely be much less burdensome, however the leisure and hospitality industries will recuperate extra slowly.

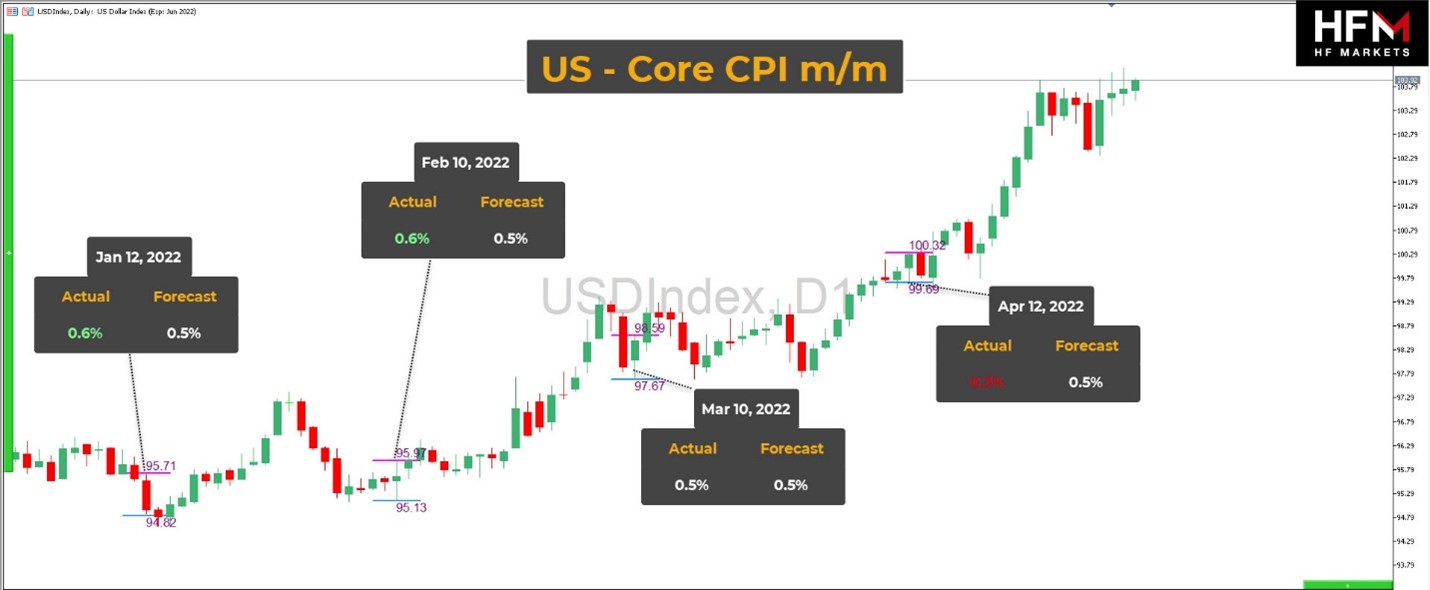

USDIndex

The 4-hour chart of the US greenback index reveals an attention-grabbing situation. The index declined and is now wobbling across the 20-period SMA. If the index doesn’t discover any help right here and falls beneath the 20-period SMA, we might even see slightly deeper correction in the direction of the 100.00 benchmark. Nevertheless, the chance of rangebound market behaviour is quite excessive.

In case of any upside pattern resumption, the multi-year excessive round 104.20 would be the key stage to look at. If the index finds resistance, it might bounce again to the 100-102 vary. Nevertheless, on a legitimate breakout, the value might soar to 105.00.

Click on right here to entry our Financial Calendar

Adnan Rehman

Market Analyst

Disclaimer: This materials is offered as a common advertising communication for data functions solely and doesn’t represent an unbiased funding analysis. Nothing on this communication comprises, or must be thought of as containing, an funding recommendation or an funding suggestion or a solicitation for the aim of shopping for or promoting of any monetary instrument. All data offered is gathered from respected sources and any data containing a sign of previous efficiency is just not a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature entails a excessive stage of threat for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made based mostly on the knowledge offered on this communication. This communication should not be reproduced or additional distribution.

{kind=link}