The S&P 500 (ASX: SPY) has been promoting off because it peaked at its all-time excessive of $479.98 on Jan. 3, 2022. Shares fell as little as $410.64 earlier than staging a bounce try. Because the pandemic lows of $218.26 set in March 2020, the “purchase the dip” technique has labored out nicely for probably the most half. Nonetheless, there’s a key purpose it’s now not working and should not work transferring ahead, larger rates of interest. The U.S. Federal Reserve has been extremely dovish with its quantitative easing (QE) pumping over $120 billion a month in asset purchases ballooning the steadiness sheet to almost $9 trillion. The “simple” cash has been a boon to buyers, and a bane to savers as rates of interest actually non-existent and a bane to shoppers as this has allowed inflation to spike to the very best ranges in 40-years at 7.5%. It is a far cry from the two% inflation price that the Fed has focused. The query is why has the Fed let inflation rise so excessive?

Depositphotos.com contributor/Depositphotos.com – MarketBeat

Depositphotos.com contributor/Depositphotos.com – MarketBeat

Transitory or Sustained?

Because of the COVID-19 pandemic and self-inflicted financial stops from lockdowns, the drop in productiveness was anticipated to be short-term. On the flipside, the snap-back restoration bounce on the reopening was additionally anticipated to be short-term because it overshoots. Exchange the phrase short-term with the time period transitory and that’s what Fed Chairman Jerome Powell was preaching all by 2021. The inflationary pressures are because of the spike in demand overwhelming the provide scarcity because of the reopening from the pandemic. It’s all short-term and can revert again to “regular”, proper? Nonetheless, the issue is that shutting down factories and manufacturing after which getting them again on-line shouldn’t be a simple or low-cost process. That is evident by the worldwide chip scarcity and provide chain disruptions we’re seeing globally. Meals, gas, and wage inflation has run amok because the U.S. has seen the quickest spike in CPI in 4 many years. The Fed has modified its rhetoric and eradicated the phrase “transitory” from its vocabulary. Since unemployment is at report lows underneath 4%, the “coast is evident” to start out financial tightening steadily.

Financial Tightening

We’ve been in a financial enlargement interval for the reason that pandemic. Now it’s time to pay the piper (again). This implies tapering down the month-to-month bond buying (QE) program and practically eliminating it in Q1 2022. It additionally means trimming the huge Fed steadiness sheet down from practically $9 trillion. Most impactfully, it means elevating rates of interest to fight inflationary pressures. The mix of all three drive the financial tightening course of designed to dampen the tempo of financial enlargement and inflationary pressures. Naturally, that is bearish for asset costs particularly shares. The inventory market strikes on rumor and resolves on information. The anticipation of rising charges and transition to a hawkish stance was evidenced by the December FOMC assembly minutes. This set-off the inventory market cliff dive in early January 2022 because the SPY fell practically 10% off its highs and Nasdaq fell 20% off its highs by the tip of February, earlier than the current bounce. There’s large hypothesis that the Fed will elevate rates of interest from 3 instances as much as 6 or 7 instances as Jamie Dimon of JPMorgan Chase commented on its earnings convention name. The underside line is larger rates of interest imply decrease markets as “danger off” stance takes impact. The Russian invasion of Ukraine is inflicting oil costs to spike and the following sanctions in opposition to Russia will affect costs for merchandise within the U.S. and globally. Whereas some speculate that the Fed could ease up on the hawkishness because of the geopolitical occasions, if the result is the acceleration of inflationary pressures, then the Fed must react even more durable to offset the expectant surge. This 12 months could very nicely be one in all enjoying protection as the entire market local weather has reversed with the Federal Reserve’s stance on rates of interest. There will probably be alternatives for buyers and merchants who administer self-discipline and endurance over panic and FOMO. Let’s check out the place probably the most opportunistic spots will probably be on the SPY.

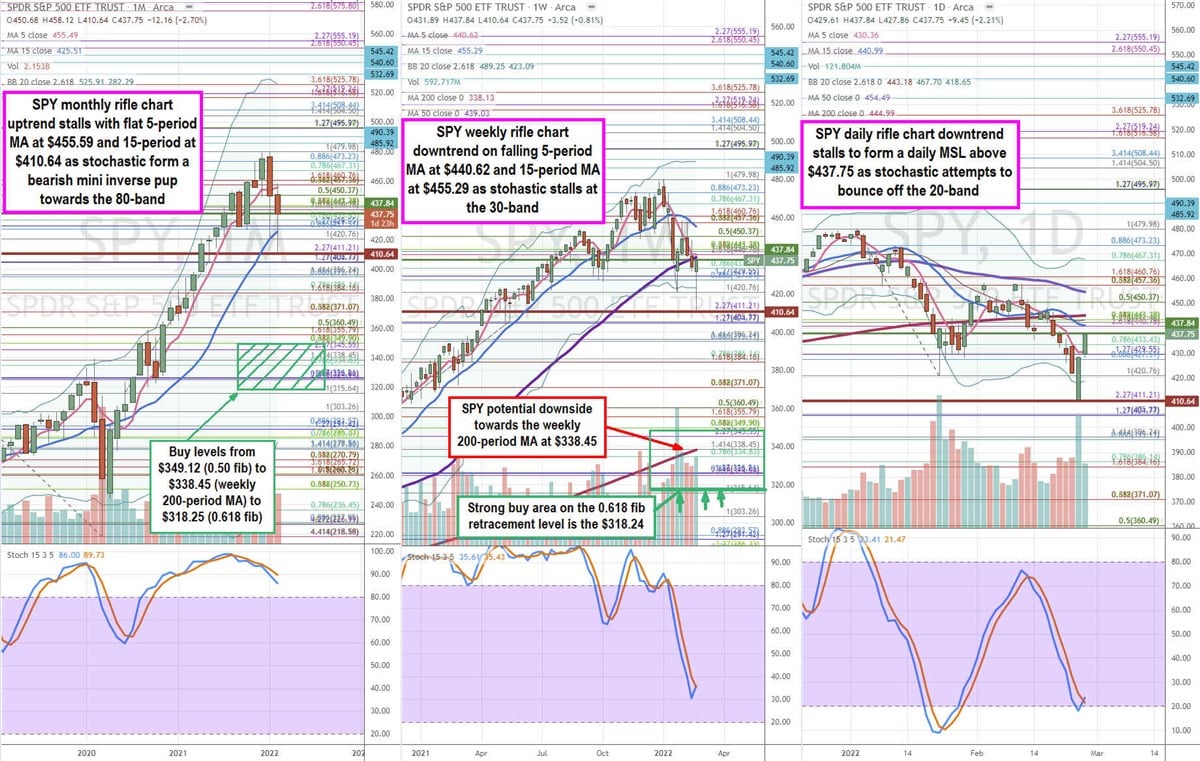

SPY Value Trajectories

Utilizing the rifle charts on month-to-month, weekly, and day by day time frames supplies a hen’s eye view of the SPY. The SPY hit a pandemic low of $218.26 on March 24, 2020, from a excessive of $337.34 on Feb. 19, 2020. The SPY proceeded to rally off the lows to a excessive of $479.98 on Jan. 4, 2022. Shares then proceeded to fall to a near-term low of $410.64 earlier than making an attempt a significant rally. Watching key Fibonacci (fib) stages utilizing the pandemic low to the post-pandemic excessive (web 261.72 factors) supplies a key 50% retracement stage at $349.12 and the 61.8% highly effective fib retracement space at $318.24, which is the final word purchase space for merchants and buyers. The month-to-month rifle chart is the widest time-frame offering the broadest and arguably the simplest view for long-term buyers. For 2 years the month-to-month rifle chart breakout uptrend lasted earlier than lastly forming a market construction excessive (MSH) promote set off on a breakdown beneath $410.64. The month-to-month stochastic has stairstep mini inverse pups however continues to be above the 80-band. If the month-to-month stochastic falls underneath the 80-band, look out beneath as a deeper oscillation might finally sell-off the market in direction of the 0.50 and 0.618 fib retracements at $349.12 and $318.24, respectively. This could usher in a bear market. These are each nice purchase/common ranges for buyers to think about scaling in lengthy positions. In the meantime, the weekly rifle chart has been in a full oscillation down falling from the 80-band to the 30-band earlier than making an attempt to cross up once more after the markets bottomed on the Russian invasion of Ukraine. The important thing resistance of the weekly 50-period transferring common (MA) is at $439.03 with the weekly 5-period MA resistance at $440.62. If the weekly stochastic manages to cross up, then a channel tightening again to the weekly 15-period MA is feasible at $455.29. Nonetheless, if the weekly stochastic coil try turns in a mini inverse pup, then an additional sell-off is feasible in direction of the 0.50 retracement space $349.12 and the highly effective weekly 200-period MA at $338.45, which coincidentally occurs to be near the pre-pandemic highs (339.08) made in 2020. The day by day rifle chart illustrates the near-term day by day market construction low (MSL) purchase set off above the $437.75 primarily based on the sturdy reversal try as stochastic coils off the 20-band. Understand that bear markets have very sharp bounces, however the wider time frames have to be saved in perspective to gauge the final market downtrend. In abstract, count on the market to bounce first on the day by day MSL triggers however the wider time-frame charts of the weekly and particularly month-to-month should be revered and used to gauge areas to promote into the bounces. The best areas to purchase is when the SPY falls right down to the $349.12 to $218.25 ranges, which represents a mess of helps together with the 0.50 fib to the 0.618 fib retracements and the weekly 200-period MA.

{kind=link}