Have you ever ever set your utility invoice to auto-pay? Cut up a dinner invoice by sending your pal money by Venmo? Had the IRS drop a pleasant, juicy tax refund straight into your checking account? If that’s the case, you’ve already skilled the advantages of ACH cost.

And also you’re undoubtedly not alone. In actual fact, 2021 noticed 29.1 billion ACH funds overlaying $72.6 trillion of worth, in keeping with knowledge from Nacha. That works out to round 87 transactions for each particular person in America. ACH funds contact our lives in so many ways in which clients now anticipate the comfort that they provide. That’s excellent news for you as a result of ACH funds also can save your online business cash and scale back the danger of fraud. ACH additionally makes it simple to supply subscriptions and recurring funds– liberating up time for each your clients and gross sales staff.

What’s ACH cost?

An ACH cost is a kind of digital transaction that transfers cash from financial institution to financial institution.

ACH stands for “Automated Clearing Home”, which is a community that connects all banks inside the USA. This connection permits the switch of cash immediately between banks, with out counting on paper checks, wire transfers, or bank card processing.

The clearinghouse is maintained and ruled by a company referred to as Nacha (previously NACHA or the Nationwide Automated Clearing Home Affiliation). Nacha additionally units the principles and rules that shield your and your clients.

Some frequent examples of ACH funds embrace:

- PayPal or Venmo

- Direct deposit payroll

- Direct deposit tax refunds

- Computerized invoice pay

ACH isn’t the one kind of digital cost although, so it may possibly get confused with different cost strategies. Let’s check out a couple of frequent questions you will have.

Is ACH cost the identical as EFT?

EFT, or digital funds switch, is a catch-all time period for any kind of digital cost. An ACH cost is one kind of EFT, however there are numerous different varieties, together with bank cards, ATMs, and wire transfers.

Is ACH cost the identical as wire switch?

Wire transfers and ACH funds are each examples of digital transactions, however they’re not the identical.

The most important distinction is that wire transfers are particular person requests that occur in real-time. ACH transactions are processed in batches at set instances all through the day. Which means funds from wire transfers are sometimes obtainable on the identical day, whereas ACH funds might take as much as 3-5 enterprise days to finish.

That prime velocity comes with a excessive price ticket although. The second largest distinction is that wire transfers common round $25 per transaction. Evaluate that to the common ACH price of round $0.29.

The final vital distinction is that ACH funds are reversible, whereas wire transfers are everlasting.

| Wire Switch | ACH Cost | |

| Cadence | Actual-time | Batched |

| Timeline | Similar day | 3-5 bus. days |

| Avg. Value | $25 | $0.29 |

| Reversible? | No | Sure |

How does ACH cost processing work?

An ACH cost begins if you ship a cost request to your financial institution or cost processor. A number of instances a day your financial institution will ship all the requests it’s gathered to an ACH operator. The ACH operator forwards your request to the receiving financial institution to confirm it. The 2 banks can now immediately deposit or withdraw the funds in keeping with the request.

Forms of ACH Cost

There are two sorts of ACH funds: credit score and debit. The distinction between them is through which course the transaction goes.

ACH Credit score – Utilized by a enterprise to “push” cash into one other checking account.

Instance: Direct deposit paychecks.

ACH Debit – Utilized by a enterprise to “pull” cash from a buyer’s checking account.

Instance: Auto invoice pay

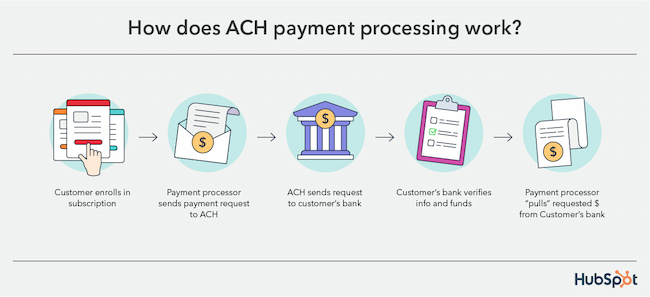

A Nearer Take a look at an ACH Cost

To higher perceive how ACH cost processing works, let’s take an instance of an ACH debit.

- Your buyer enrolls in a month-to-month subscription. They provide you their checking account data and cost authorization.

- When cost is due, your cost processor sends a request to the clearinghouse. (In Nacha phrases your processor is the Originating Depository Monetary Establishment or ODFI.)

- The clearinghouse processes that request as a part of a batch of requests after which sends it to your buyer’s financial institution. (Your buyer’s financial institution is the Receiving Depository Monetary Establishment or RDFI.)

- Your buyer’s financial institution receives the request and verifies that your buyer’s data is correct. And that they come up with the money for to cowl the invoice.

- If all the pieces checks out, your buyer’s financial institution (the RDFI) permits your processor (the ODFI) to “pull” the requested funds.

An ACH credit score works the identical approach, besides that the ODFI “pushes” the cash to the RDFI as an alternative.

How lengthy do ACH funds take?

ACH funds sometimes take between 3-5 enterprise days to finish. Nacha guidelines name for ACH debits to be processed by the following enterprise day, and ACH credit in 1-2 enterprise days. That mentioned, the timeline depends upon what time of day your batch was despatched. The receiving financial institution may maintain the funds so long as they’re allowed for safety causes.

Some ACH funds could also be eligible for same-day, next-day, or 2-day processing, however this may bump up the fee.

Is ACH cost secure?

In keeping with a research executed by the Federal Reserve, ACH funds have the bottom fee of fraud by worth, averaging solely $0.08 of fraud for each $10,000. That makes ACH safer than bank cards, debit playing cards, and even ATM withdrawals.

That’s as a result of Nacha has strict guidelines and tips for danger administration. These guidelines require all banks or companies concerned to take “commercially cheap” steps to confirm buyer data and shield delicate knowledge.

That mentioned, “cheap” can imply various things for various companies. It’s vital to be sure that your cost processor makes use of up-to-date safety measures.

For instance, HubSpot funds ensures all cost credentials are each encrypted and tokenized. By utilizing a number of layers of safety, your clients can belief that you simply’re conserving their delicate data protected.

How a lot does ACH cost value?

Nacha doesn’t set the charges related to ACH funds, so the fee depends upon the financial institution or cost processor you employ.

Some processors cost a flat price, which usually ranges from $0.20 to $1.50 per transaction. Others might cost a proportion of the transaction quantity, and this typically falls between 0.5% to 1.5%.

Third-party processors may cost further charges upfront or month-to-month to make use of their service, so be sure to’re evaluating all prices when selecting a supplier.

With HubSpot funds, you pay 0.5% of the transaction quantity, with a cap of $10 per transaction. There are not any month-to-month charges, setup prices, or hidden prices, so that you solely ever pay for the service if you want it.

Is ACH cost proper for your online business?

Whether or not ACH is best for you comes right down to the wants of your online business. An organization that depends on month-to-month billing can save some huge cash by utilizing ACH as an alternative of bank cards. Alternatively, ACH might not make sense for a retailer with out numerous repeat clients.

Listed here are a couple of causes you may use – or not use – ACH funds.

When to Use ACH

- Your enterprise entails recurring funds or subscriptions.Accepting ACH funds means your clients don’t have to recollect to dig out their wallets each month.

- You’re uninterested in sending paper invoices. ACH funds are dealt with completely on-line. In actual fact, HubSpot funds lets you settle for cost straight from your individual web site. Or create safe, shareable cost hyperlinks that your clients can entry by telephone, e mail, and even on-line chat.

- It’s essential save on bank card charges. Bank card processing charges usually run 2-3% or extra.

- Your clients’ funds are getting declined. ACH funds come immediately out of your clients’ financial institution accounts. This implies fewer rejected funds than bank cards, which may expire or get misplaced or stolen.

- Your clients’ safety is a prime precedence. ACH funds expertise much less fraud than some other cost processing methodology.

When to Not Use ACH

- You’ve gotten numerous worldwide clients. Though ACH will nonetheless work nice for patrons within the U.S. or U.S. territories.

- Your clients must make high-dollar funds.Though Nacha has raised the per-transaction restrict to $100,000, your financial institution or cost processor might impose their very own limits.

- You may’t wait 3-5 enterprise days for cost. ACH funds are slower than bank card processing or wire switch.

How you can Settle for ACH Cost

If you wish to begin accepting ACH funds frequently, you’ll wish to work with a third-party cost processor. When you can deal with ACH transactions by your financial institution, they seemingly received’t give you a safe methodology of gathering your clients’ account data.

Gross sales Hub customers can join ACH transactions in minutes, and sometimes begin accepting funds inside 1-2 enterprise days.

And HubSpot funds integrates immediately together with your CRM, so your clients could make safe funds straight by your web site, e mail, or on-line chat. Or put safe, shareable hyperlinks proper into your quotes.

Leveraging ACH Funds for Your Enterprise

In fact, selecting ACH funds isn’t an either-or determination. Many cost processors, together with HubSpot, mean you can settle for ACH and bank cards from the identical instrument. Providing your clients a number of cost choices makes it simpler for them to make a purchase order. And meaning extra money in your financial institution.

{kind=link}